Introduction

Risk parity (equal risk) investing was pioneered in the 1990s. It gained traction with large institutional investors during the early 2000s, and became even more popular after the 2008 financial crisis, when the strategy delivered strong relative performance. The general idea is to construct an investment portfolio that can perform fairly well in any economic environment. While the basic concept is simple, the actual mechanics of implementing it can get quite complicated. At Bernstein Financial Advisory, we have developed a modified version of this strategy that offers many, but not all, of its benefits in a way that is suitable for the average individual investor – the Better-Balanced Portfolio.

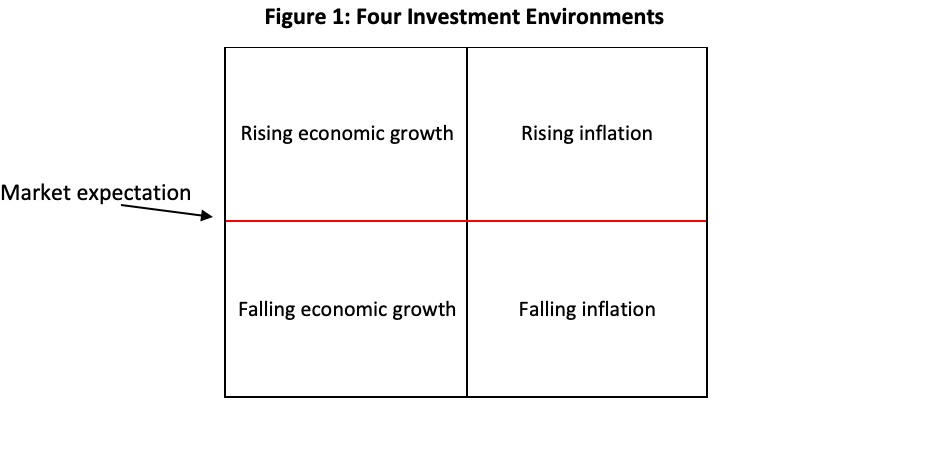

Four Investment Environments

When considering the most effective way to diversify an investment portfolio, it’s important to start by thinking about the four basic investment environments that exist: rising economic growth, falling economic growth, rising inflation, and falling inflation as shown in Figure 1.

Certain types of assets perform best in one or two of these environments, but perform poorly in the others. A simple example is equity (stocks). Equity performs well in times of rising economic growth and/or when there is falling inflation, but most equity performs poorly in the other two environments (falling economic growth and rising inflation).

Risk: Why Should I Care?

For our purposes, we will define risk as the possibility that a given asset (stocks, bonds, etc.) will lose value. This loss of value could be for a short period of time, such as the pandemic stock market correction that occurred from February 2020 to August 2020, an intermediate period like the 2008 financial crisis that lasted from December 2007 to December 2010, or an extended period like the Great Depression, which began in September 1929 and did not recover until July 1956. The beginning dates used above are based on the S&P 500 Index high, right before each correction started, and the end dates are the point at which the index recovered to that same pre-correction level.

In each of these three examples, stocks lost value for 6 months, 3 years, and 27 years, respectively. Depending on your need to access (sell) those assets during the period that they lost value, this could result in a permanent loss of wealth. It is this type of risk, particularly the longer duration examples, that diversification seeks to at least partially offset.

Portfolio Diversification

In an ideal world, we would simply shift between the assets that perform best in each environment just before the rest of the market does the same to capture the positive return. Of course, if this were possible portfolio diversification would be unnecessary, since we would correctly time the shift between assets just before each change in investment environment. If we had this figured out, I wouldn’t be writing this article, or, at a minimum, I’d be dictating it to my private secretary from the beach on my private island in the Caribbean!

Fortunately, there is a more reasonable alternative to the above that does not require a Magic 8 ball. Instead of trying to correctly time the shifts between investment environments, we can distribute the risk in your portfolio more evenly between assets that will perform well in each of the four environments.

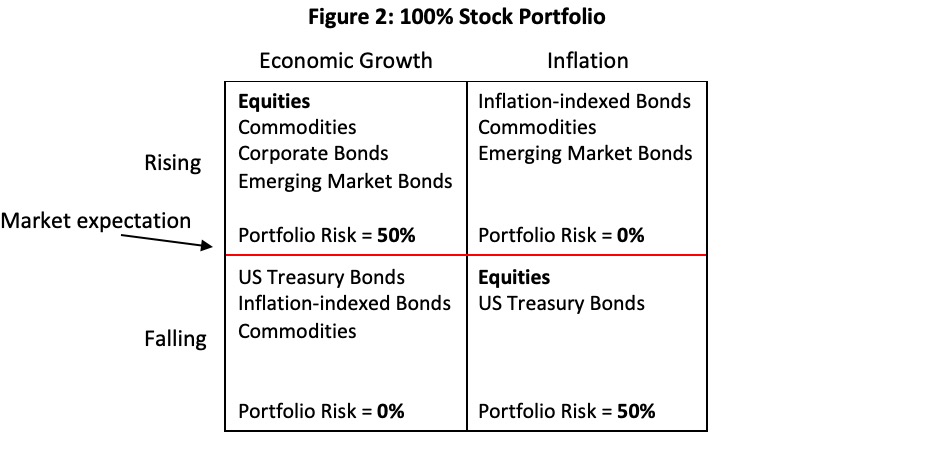

Let’s use a simple example. We’ll start with a portfolio that is 100% equity. As mentioned earlier, equity performs well in two of the four environments. Figure 2 shows the same four investment environments displayed in Figure 1, as well as the assets classes that perform best in each. In our example of a portfolio that is invested completely in equities, you can see that the risk is evenly distributed between two of the four environments, but there is no exposure to the remaining two (falling economic growth and falling inflation).

60/40 Portfolio

Most investors understand that having a portfolio of all equities is riskier than a portfolio that also holds other assets. The most commonly used strategy to diversify the risk of an equity portfolio is a mix of stocks and bonds, typically 60% stocks and 40% bonds. We’ll call this the 60/40 portfolio.

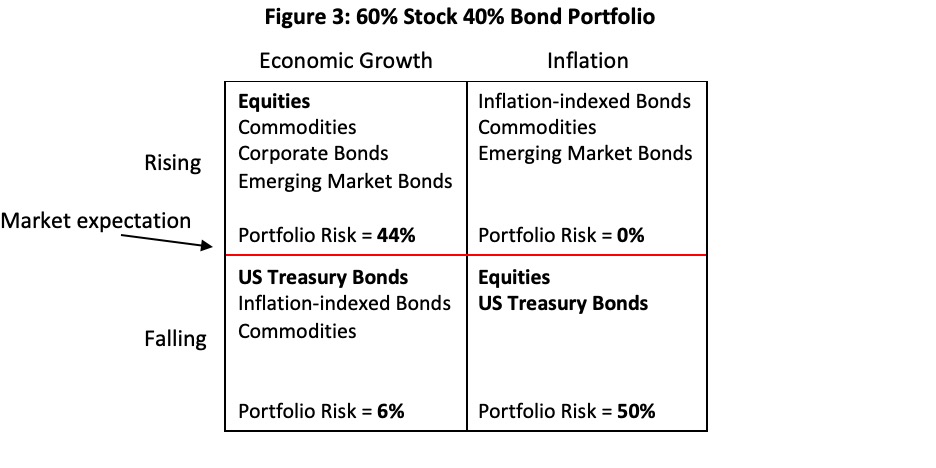

There are several problems with this approach. The first is that the assets are most commonly allocated based on their dollar value in the portfolio, instead of each asset’s contribution to the risk in the portfolio. Since stocks are roughly five times as risky as Treasury bonds, the risk is distributed much differently than the 60/40 implied by the allocation using dollar amounts. Figure 3 shows the portfolio risk distribution of a typical 60/40 portfolio that has been allocated based on the dollar value of the assets.

As displayed above, shifting to a 60/40 portfolio based on dollars does very little to distribute the risk more evenly, compared with the 100% stock portfolio that is displayed in Figure 2. Just 6% of the risk shifts from rising economic growth to falling economic growth. Again, this is because Treasury bonds are about one-fifth as risky as stocks.

The second problem is specific to the current interest rate environment. As most people know, interest rates are near record lows. Most of us are very aware of the minuscule interest earned in a bank savings account, or the very low interest rate paid on a mortgage.

Generally speaking, the value of a bond rises as interest rates fall, and the value of that same bond decreases as interest rates rise. With interest rates at record lows, it will be difficult for them to fall much more. There is a much higher probability that interest rates will rise over the medium to long term, which will decrease the value of a bond.

As a result of these factors, the bottom line is that a traditional 60/40 portfolio is likely to be very ineffective at diversifying the risk of an equity portfolio. That’s the bad news; the good news is that there are other assets that can effectively diversify the risk of a stock portfolio. They are displayed in Figures 2 and 3 above.

Risk Parity Portfolio

A perfectly balanced risk parity (equal risk) portfolio would have 25% of the portfolio risk in each of the four possible investment environments. One of the most basic rules of investing is that higher risk typically yields higher return, and lower risk typically generates lower return. As mentioned earlier, Treasury bonds are much less risky than stocks. However, that means over time, the return on those bonds is also lower than it is for stocks.

To account for this, a well-balanced risk parity portfolio uses leverage to make up for the difference in returns. In other words, purchases of lower return assets, like bonds, are increased by borrowing money. This can increase the returns from these assets, but it can also increase the losses. There are good reasons to do it, but it adds a level of complexity that is probably not appropriate for the average investor.

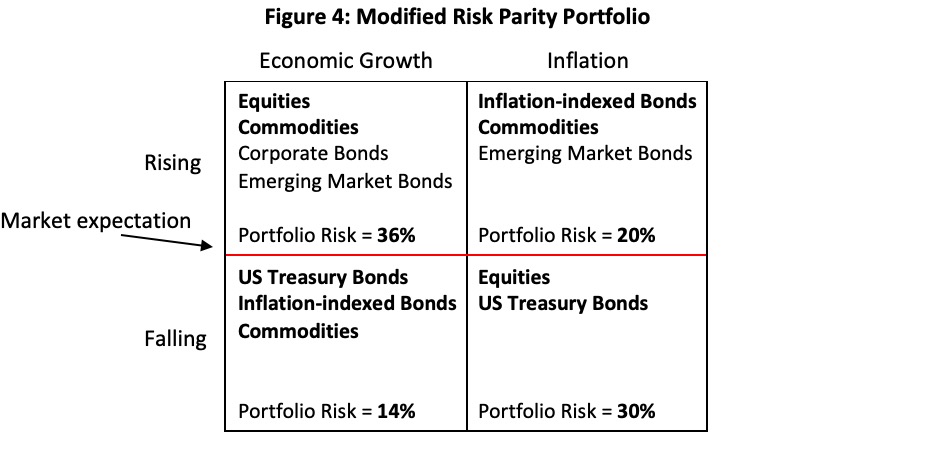

Modified Risk Parity Portfolio

A modified risk parity (equal risk) portfolio uses all of the principles that I have described above, but does not use leverage. We call this the Better-Balanced Portfolio. The concept is to distribute the portfolio risk more evenly between the four investment environments without using leverage (borrowing money). These modifications can also include custom tailoring of your portfolio to match your personal risk tolerance. In other words, the contribution to portfolio risk from stocks (not dollars invested in stocks) can be adjusted to any level.

Conclusion

There are some important basic concepts to understand about the Better-Balanced Portfolio. This portfolio should provide better protection through all four of the possible investment environments compared with a portfolio that is more concentrated in assets that only perform well in some of those environments. That also means that it will not do as well as a portfolio that has higher exposure to a specific environment when that particular environment is in favor.

Specifically, in a bull market when stocks are doing well, the Better-Balanced Portfolio will not do as well as a 100% stock portfolio, or a 60/40 portfolio. Of course, this also means that when we are not in an environment that is positive for equities, the Better-Balanced Portfolio should perform more favorably. In addition, the Better-Balanced Portfolio eliminates the need to attempt to forecast shifts between environments because the risk is distributed to provide at least some protection in each possible investment environment.

If you would like to discuss implementing a Better-Balanced Portfolio with your investments, please contact us by email, phone, or by clicking the “Let’s Talk!” button at the top of this page to schedule a complimentary introductory meeting.